Small business lending is critical to the financial industry, vibrant communities, and the American economy. However, lending institutions face challenges in increasing small business lending while managing credit risk and allocating resources. To address these challenges, it is essential to streamline lending processes, improve operational efficiency, manage risk effectively, and boost profitability. The Lumos Business Report is a powerful solution that uses automated intelligence and machine learning to provide valuable insights and efficiency for small business lending.

Strict requirements and manual underwriting processes create inefficiencies in the early stages of a loan opportunity. Lenders often have many leads to sift through, and due to the amount of work and inefficient nature of filtering through them all, many deals end up getting missed or dropped. On top of this, there is often a mismatch between the information obtained in the early stages of the relationship and the information used to assess the risk profile, provide pricing, and make a loan decision.

It is easy to feel the friction of promoting the growth of the commercial loan portfolio while managing credit risk within prescribed parameters, achieving growth, and increasing profitability. And the problems are not entirely internal to a financial institution (FI). Small businesses often do not seek or obtain financing from their primary service provider.

Internal Challenges:

- Lack of automation, especially in the early stages, resulting in a slow small business loan origination process

- Credit risk profile not including real-time information and economic data

- Decreased productivity and profitability across the lending and credit teams

- No transparency and inconsistencies among lending and credit teams

External Challenges:

Ninety percent of businesses use banks as a financial services provider but…

- 32% of businesses do not seek financing from banks due to strict lender requirements.

- 24% of businesses do not seek financing from banks due to lenders not working with businesses like theirs.

- Businesses frequently claim that their business is too small, too new or their industry too risky to qualify for financing.

Extensive manual hours are required early in the lending process to properly prescreen an opportunity. Manual prescreens may be inconsistent, inadequate, or inefficient resulting in lost productivity or time wasted when the loan does not progress. The early stage assessment can involve web searches for news articles or updates on the business or borrower to identify any apparent red flags, introductory conversations with the borrower to delve into the loan request, requirements and experience, data gathering from various sources and combining it into one analysis that leads to next steps, internal discussions with various departments within the organization to identify action items and a game plan for the request, and utilizing third party sources to gather data on the borrower that was not readily available upon request. It’s a lot! It’s time-consuming. It’s costly.

Fortunately, data insights and automation allow FIs to efficiently navigate these conflicting challenges within small business lending. Most loan inquiry forms are simple with limited information required, such as use of proceeds, requested loan amount, estimated FICO score range, and industry. However, to make a final credit decision, most institutions require significantly more detailed information such as business plan, ownership structure, financials, collateral detail, hard credit score, existing debt, credit history, bankruptcies/delinquencies, and economic impact. The incorporation of predictive credit models and AI-driven technologies can significantly increase productivity and allow FIs to better serve the drivers of the American economy and their own growth and profitability.

The Solution

With the Lumos Business Report, FIs can optimize their lending processes with intelligent data extraction and automation, manage risk with actionable insights and enable strategic growth, ensure consistency in decision making and risk analysis, enhance teams with automated intelligence, and boost profitability with efficiency, loan growth, and risk-informed pricing.

The Lumos Business Report is two generative AI products rolled into one – the Business Report and the Qualification Grade.

The Business Report

With generative AI from Lumos, FIs can quickly capture various topics such as an overview of the business, industry overview, operations, sales and marketing strategy, customers, partnerships, strengths and weaknesses, and the team or operators of the business with just a few relevant data points. The report provides benchmarks and data on the loan opportunity industry comparisons, top lenders, loan size, loan pricing, and economic factors. The benchmarks and data are derived from three decades of SBA loan performance data and current economic conditions, all easily delivered by a large language model.

The Qualification Grade

With just a few relevant data points about a small business loan opportunity, FIs can generate the Lumos Business Report and the Lumos Qualification Grade in less than 30 seconds. The Lumos Qualification Grade incorporates multiple business and economic factors to display an opportunity’s probability of default, loss given default, and expected loss. Plus, there is no concern about privacy issues, as the inputs do not include any personal information.

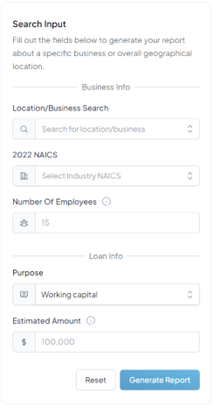

The Lumos Business Report helps FIs evaluate the credit risk and performance of small businesses that are seeking loans. Users input five items of information about the business and the loan:

- Business name and location

- NAICS code

- Number of employees

- Use of proceeds

- Estimated loan amount

After generating the report, users will receive a comprehensive summary of the business and the loan, including:

- Business and loan overview

- Address and industry sector

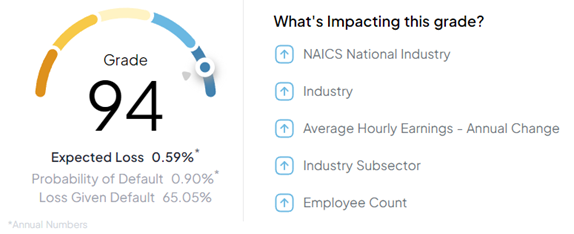

- Qualification Grade

- Top 5 factors influencing the credit grade and their impact

- Business write-up using natural language processing

- Credit benchmarks and data

- Economic overview and factors

The Qualification Grade is a unique feature of the Lumos Business Report that uses Lumos’ dataset of more than two million SBA loans with robust loss data including over 400 thousand defaults and 300 thousand charge-offs to calculate PDs, LGDs, and ELs. The data spans three decades of loan and macroeconomic data covering the Dotcom Crash, Great Recession, and economic turbulence of 2020.

This Qualification Grade ranges from 0 to 100, with 100 being the least risky, and is based on both the probability of default and loss given default. The report also identifies the five most impactful factors on expected loss for this specific business and whether each factor increases or mitigates risk.

The business write-up uses natural language processing to generate a concise and informative summary that covers multiple topics such as an overview of the business, industry overview, operations, sales and marketing strategy, customers, partnerships, strengths and weaknesses, and the team or operators of the business. This information is sourced directly from public domains such as the business’s website and other major sources, which are typically used by lenders and underwriters to analyze a business on the front-end. Using a large language model, this information is summarized into an easy-to-use format.

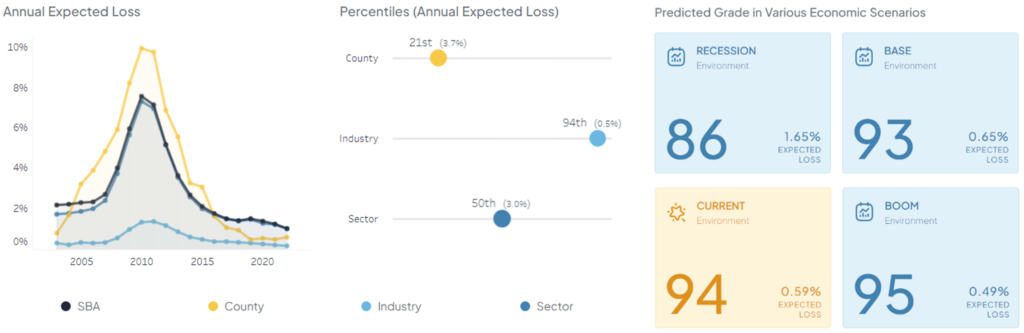

The Lumos Business Report covers benchmarks and data. The predictive model is built on nearly thirty years of SBA loan performance data, which is used to benchmark this opportunity relative to others historically. This includes comparisons of the industry to the sector, county, and overall SBA in terms of expected loss and percentiles.

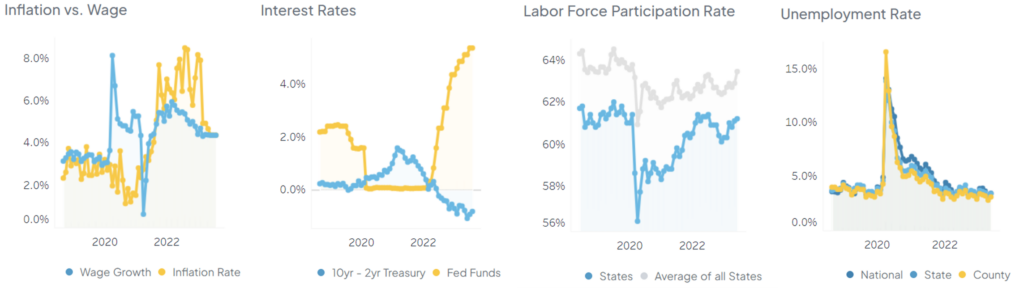

An economic overview of the opportunity is also provided, showing how current economic conditions impact risk compared to a recessionary, base, or booming environment. Economic factors such as inflation, interest rates, wages, unemployment, and labor force are included in the analysis to provide further insight for both the lenders and borrowers.

The Lumos Business Report shows top lenders in this space, average loan size, gross approvals, and market share of top lenders broken down by county, sector, and industry. Loan pricing trends are also included, showing how loans of similar sizes are being priced across similar counties, sectors, and industries.

The Lumos Business Report provides a detailed and transparent overview of the business and the loan using advanced data analysis and natural language processing techniques. Lumos delivers a state-of-the-art machine learning qualification model with comprehensive validation. The model risk management process follows modeling best practices and is aligned with FDIC and OCC regulatory guidelines. The Lumos Business Report is based on verified and legitimate sources of information gathered from the public domains and insights from Lumos’ proprietary small business loan dataset.

Lumos Business Report is a powerful solution for small business lending that uses cutting-edge machine learning algorithms and proprietary data to provide valuable insights and automation. Incorporating predictive credit models and AI-driven technologies bridge the gap between limited front-end information and making a final credit decision in small business lending. The Business Report and Qualification Grade will improve productivity and efficiency for FIs that want to assess the viability and potential of small businesses loan opportunities.