It’s not a secret that financial institutions have historically struggled to provide small dollar financing to small businesses. This type of lending comes with inherently higher risks and returns that hardly justify the operational costs. An institution that overcomes these hurdles has taken the first steps toward a tremendous market opportunity – 33 million small businesses in the United States. While there have been efforts to address the struggle and capture the opportunity, lending to the smallest of small businesses remains elusive and not ideal.

The Struggle

Financial institutions have two primary problems to overcome for small dollar small business lending:

- Operational costs for originating and servicing

- Increased credit risk for loans less than $500 thousand

Small dollar small business lending requires a significant reduction in operating costs to be a viable business within a financial institution. To achieve a similar efficiency as larger dollar small business loans, lenders must reduce operating costs over 6x on average.

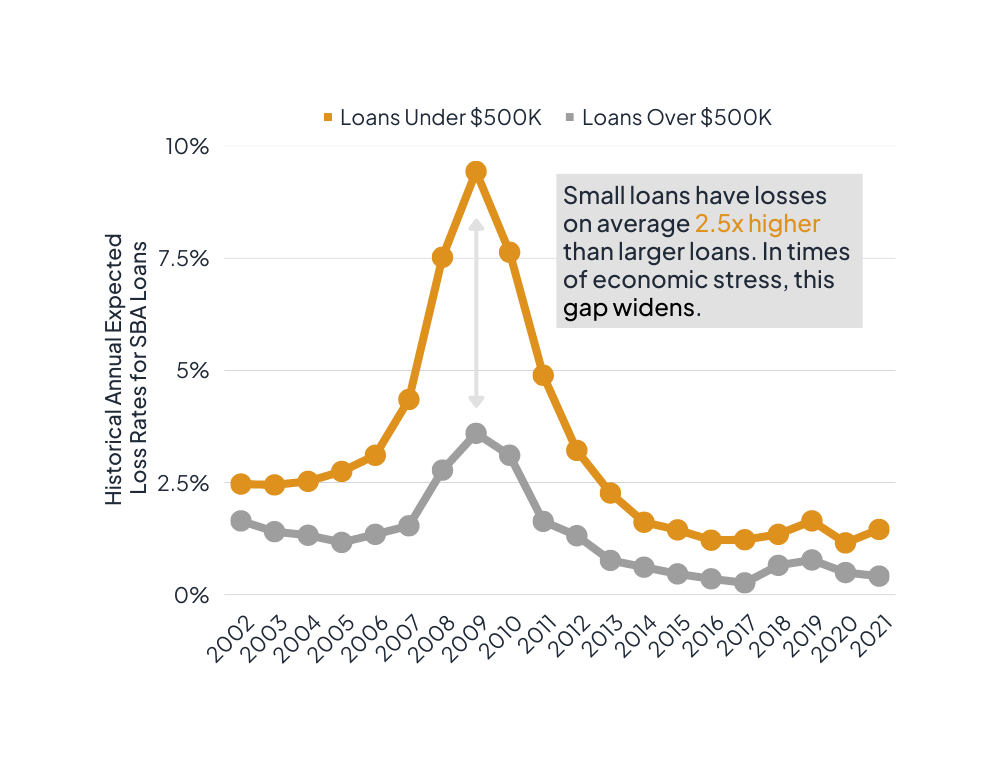

In addition to punitive and disproportionate operational costs, small dollar small business loans also come with greater risk of loss for the financial institution. On average, the risk of loss on loans less than $500 thousand to a small business is 2.5x higher than larger loans. Furthermore, the comparative losses for smaller loans increases during times of economic stress.

The Struggle

Financial institutions have two primary problems to overcome for small dollar small business lending:

- Operational costs for originating and servicing

- Increased credit risk for loans less than $500 thousand

Small dollar small business lending requires a significant reduction in operating costs to be a viable business within a financial institution. To achieve a similar efficiency as larger dollar small business loans, lenders must reduce operating costs over 6x on average.

In addition to punitive and disproportionate operational costs, small dollar small business loans also come with greater risk of loss for the financial institution. On average, the risk of loss on loans less than $500 thousand to a small business is 2.5x higher than larger loans. Furthermore, the comparative losses for smaller loans increases during times of economic stress.

For years, financial institutions have relied heavily on consumer credit or small business credit scores to understand small business risk. The name itself implies that consumer credit scores have limited applicability to credit worthiness of a small business. But, this limitation hasn’t interfered with the overly broad application of the owner’s consumer credit score for small business lending. Consumer credit scores provide minimal contribution to probability of default (PD) predictions and do not contribute anything to loss given default (LGD) predictions. Unfortunately, current leading business credit scores do not perform better than consumer credit scores for assessing risk. Business scores are often built using different loan types, different market segments, and data not available for smaller and newer businesses. This significantly diminishes the accuracy of these scores for small dollar small business lending.

The problems for financial institutions in turn create problems for small businesses. According to the Federal Reserve’s 2022 Small Business Credit Survey, 65% of the smallest and newest small businesses do not receive any of the requested financing from lenders. Faced with limited alternatives, small businesses will often turn to nonbank lenders and accept unfavorable loan terms to meet capital needs. This creates a considerable opportunity for banks to serve the needs of its small business community.

The Opportunity

There are over 33 million small businesses in the United States. On average for the past five years, more than 2.2 million businesses have applied each year for a business loan, a business line of credit, or an SBA loan. Small businesses are looking for:

- Favorable loan terms

- Fair and tolerable interest rates

- Timely credit decisions from the lender

- Convenient application processes

With improvements in technology and data-driven insights for credit underwriting, banks are very well positioned to deliver on each of these. Currently, banks are better positioned to offer favorable loan terms and interest rates but fall short, compared to online lenders, in the ability to offer convenient application processes and timely decisions or funding. Generally, banks are losing market share to online lenders because of technology and underwriting processes.

Small banks are currently better positioned to close the gap with online lenders, compared to larger bank competition, while better serving their communities. Small businesses drive two-thirds of net new jobs and play a significant role in innovation and competitiveness in the United States. It is easy to see the reciprocal benefits of banks playing an active role in fostering small business growth.

There are over 33 million small businesses in the United States. On average for the past five years, more than 2.2 million businesses have applied each year for a business loan, a business line of credit, or an SBA loan. Small businesses are looking for:

-

Favorable loan terms

-

Fair and tolerable interest rates

-

Timely credit decisions from the lender

-

Convenient application processes

With improvements in technology and data-driven insights for credit underwriting, banks are very well positioned to deliver on each of these. Currently, banks are better positioned to offer favorable loan terms and interest rates but fall short, compared to online lenders, in the ability to offer convenient application processes and timely decisions or funding. Generally, banks are losing market share to online lenders because of technology and underwriting processes.

Small banks are currently better positioned to close the gap with online lenders, compared to larger bank competition, while better serving their communities. Small businesses drive two-thirds of net new jobs and play a significant role in innovation and competitiveness in the United States. It is easy to see the reciprocal benefits of banks playing an active role in fostering small business growth.

The Solution

Banks need a reliable scoring method to increase underwriting efficiency for small dollar small business loans and a digital solution that reduces the origination and servicing burden while improving the borrowing experience. The partnership between Lumos Technologies and Lenders Cooperative provides this solution. The Lumos Prime+ Score predicts expected credit losses over the subsequent twelve months for small business term loans and lines of credit under $500 thousand.

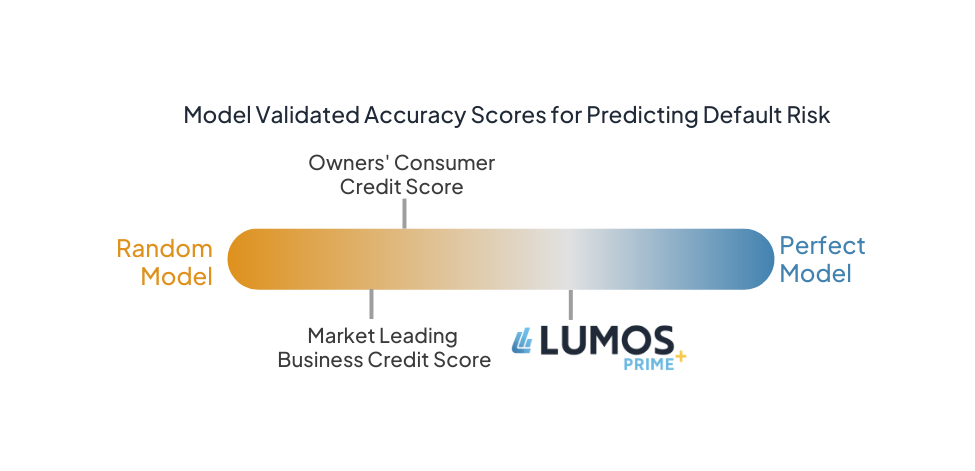

Lumos Prime+ uses three decades of small business loan performance data combined with machine learning algorithms to deliver PD and LGD predictions that are more accurate and fairer. The product of PD and LGD, the expected loss (EL) is the best indicator of the financial implication of credit risk for a bank. Back testing Lumos’ data set of three decades of performance on two million small business loans through multiple economic cycles shows that 69% of all performing loans would have received a Lumos Prime+ Score above 80. At 69%, Lumos Prime+ outperforms other market leading scores which only predict approximately 50% of performing loans.

Lumos Prime+ uses three decades of small business loan performance data combined with machine learning algorithms to deliver PD and LGD predictions that are more accurate and fairer. The product of PD and LGD, the expected loss (EL) is the best indicator of the financial implication of credit risk for a bank. Back testing Lumos’ data set of three decades of performance on two million small business loans through multiple economic cycles shows that 69% of all performing loans would have received a Lumos Prime+ Score above 80. At 69%, Lumos Prime+ outperforms other market leading scores which only predict approximately 50% of performing loans.

Additionally, the Lumos Prime+ score significantly outperforms other scoring models that give loans a passing score that are ultimately non-performers.

Lumos Prime+ returned an acceptable score for 4% of all non-performing loans in the data set. With other scoring models, this can be as much as one-third of the passing loans end up defaulting. With Lumos Prime+, banks can expect a score that expands lending by approving a greater number of small business loans that will perform while reducing the number of loans that pass through that ultimately will not perform. Simply, banks can say “YES!” more often with confidence when using the Lumos Prime+ Score.

Additionally, the Lumos Prime+ score significantly outperforms other scoring models that give loans a passing score that are ultimately non-performers.

Lumos Prime+ returned an acceptable score for 4% of all non-performing loans in the data set. With other scoring models, this can be as much as one-third of the passing loans end up defaulting. With Lumos Prime+, banks can expect a score that expands lending by approving a greater number of small business loans that will perform while reducing the number of loans that pass through that ultimately will not perform. Simply, banks can say “YES!” more often with confidence when using the Lumos Prime+ Score.

Operational Efficiency

The partnership between Lumos and Summit Technology Group (STG) delivers Prime+ through STG’s Lenders Cooperative loan origination system. Users of the Lenders Cooperative loan origination system will have initial exclusive access to the Lumos Prime+ Score enabling banks to overcome two major struggles with small dollar small business lending. Lumos Prime+ mitigates higher credit risk while Lenders Cooperative reduces the operating costs of loan origination while maintaining a focus on quality service. Lenders Cooperative’s online origination system provides end-to-end automation from digital online applications through closing and core integration. The Lenders Cooperative platform and workflow support small business C&I portfolios, SBA lending, and commercial lending products with full spreading tools, templates, and an innovative credit model.

Fairness Score

Lumos Prime+ makes small business loans more accessible and has undergone rigorous bias and fairness testing to ensure it does not indirectly have unintended disparate impacts. Using an example from the U.S. Equal Employment Opportunity Commission, Lumos Prime+ achieves the threshold for excellence in fairness using the proportional parity metric.

S.O.S - Struggle. Opportunity. Solution

Financial institutions are well aware of the struggles and the opportunities of small dollar small business lending. However, capturing the opportunity is not without hurdles. From higher credit risk to lending inefficiency, serving the smallest of small businesses requires different tools and processes than financing larger businesses. Fortunately, a packaged solution from the partnership between Lumos Technologies and Lenders Cooperative allows bankers to efficiently and effectively focus on small dollar business lending. Bankers can get back to doing what they do best – serving their customers and communities.